Medicare tax is a federal payroll tax that contributes to Medicare funding. All U.S.-based workers are required to pay Medicare tax on their wages. In accordance with the Federal Insurance Contributions Act (FICA), the tax is grouped together. When reviewing your paycheck, the Medicare tax and Social Security tax may appear as a single deduction for FICA.

The Medicare tax was established in 1966 to solve a health care problem: after retirement, the income of many seniors declines while their health care needs increase. Before Medicare, however, the cost of insurance became unmanageable, and some retirees’ policies were terminated due to their age. There are numerous components to the Medicare program, but at the time, the working population was required to pay a new Medicare tax to support Medicare hospital insurance. Below we’ll take a look at how Medicare taxes work.

How Medicare Tax Works

Medicare tax is a two-part tax: a portion is automatically deducted from your paycheck, and the other portion is paid by your employer. The tax is based on “Medicare taxable wages,” which is calculated by subtracting pretax health care deductions such as medical insurance, dental, vision, and health savings accounts from your gross pay.

Your employer is required to collect tax, and it electronically deposits both the employee and employer versions to the IRS on a regular basis. Self-employed individuals pay a Medicare tax as part of their self-employment tax. Instead of being deducted from a paycheck, the money is paid quarterly through estimated tax payments.

Medicare Tax Rate

When the Medicare tax was first introduced in 1966, the tax rate was 0.7% of an employee’s wages, with the employer and employee each paying 0.35%. The rate has since gone up considerably. In 2023, the Medicare tax rate is 2.9% which is still shared equally between the employer and employee. W-2 employees pay 1.45% towards the Medicare tax and their employer covers the remaining 1.45%. Self-employed individuals must pay the full 2.9% in full because they are both the employee and the employer.

Medicare Surtaxes

To fund the Medicare expansion, the Affordable Care Act imposed 2 Medicare surtaxes in 2013: The additional Medicare tax and the net investment income tax. Both surtaxes apply to high-income earners and are specific to distinct income types. It is possible to be subject to both of these surtaxes.

Additional Medicare Tax

The additional Medicare tax only applies to income above $200,000 ($250,000 for joint tax filing and $125,000 for married taxpayers filing separately). The additional Medicare tax rate is 0.9%. For example, if you earn $225,000 per year, the first $200,000 is subject to the standard 1.45% Medicare tax, while the remaining $25,000 is subject to the 0.9% additional Medicare tax. Similar to the initial Medicare tax, the surtax is withheld from an employee’s paycheck or paid through self-employment taxes.

Net Investment Income Tax

The net investment income tax, also known as the “unearned income Medicare contribution surtax”, imposes an additional 3.8% tax on net investment income as of 2023. As with the additional Medicare tax, no employer contribution is required. Net investment income can include taxable interest, dividends, nonqualified annuities, capital gains, and rental income. It excludes income that is already excluded for income tax purposes, such as interest on tax-exempt municipal bonds.

Net investment income tax is applied to your net investment income or the excess modified adjusted gross income (MAGI) over certain thresholds, whichever is less. Suppose, for example, that a married couple joint filing earned $225,000 in pay. The couple received an additional $50,000 in investment income during the same year, bringing their MAGI to $275,000. The tax threshold on net investment income for married couples filing together is $250,000. The couple would pay the 3.8% tax on the lesser income which would be the excess MAGI at $25,000 and not the total investment income which was $50,000. In this situation the couple would owe $950 in net investment income tax (3.8% x $25,000).

What Is The Medicare Tax Used For?

The Medicare tax funds Medicare Part A, which provides health insurance for those 65 and older, those with disabilities, and those with certain medical conditions. Medicare Part A, also known as hospital insurance, pays for hospital stays, skilled nursing care, hospice care, and certain home health services. The tax collected for Medicare accounts for 88% of Medicare Part A’s total revenue.

What Is The Additional Medicare Tax Used For?

The additional Medicare tax paid by high-income earners is used to offset the costs of the Affordable Care Act, according to the IRS. The funds are used to pay for provisions of the ACA, including the provision of tax credits for health insurance, to make health insurance more affordable for over 9 million individuals.

What Is The Medicare Trust Fund?

Medicare trust funds are what provides the money to fund Medicare beneficiaries. It is primarily made up of 2 funds:

Hospital Insurance Trust Fund (HI) – This fund finances Medicare Part A, which covers hospital stays, skilled nursing facilities, and hospice care for eligible beneficiaries. The fund’s primary sources of revenue are payroll taxes and Social Security benefits taxation. In addition, this fund and the Railroad Retirement account contribute to the annual revenue.

Supplemental Medical Insurance Trust Fund (SMI) – This fund finances Medicare Part B, which covers physician services, essential medical supplies, and a portion of the more recent Medicare Part D prescription drug program. This fund’s primary revenue source is beneficiary premiums, and it does not require a sizable amount of reserves.

Can I Opt Out Of Medicare Tax?

A religious exemption is possibly the most common way to avoid paying FICA tax. Members of recognized religious organizations that oppose accepting Social Security benefits are permitted to opt out. Although the rules and reporting requirements are very strict. The IRS outlines the rules, including the need to submit forms 4631 and 8274. So, don’t get any ideas about starting a religion just to avoid these taxes. The religious organization must have existed since 1950 and be able to demonstrate that its members have a sufficient standard of living during that time.

There are additional, even less likely ways to afford paying FICA. In some cases, these include nonresident aliens and income from student employment. The student exemption only applies to the student’s school-related employment. They must also be enrolled in the school where they work for their income to be exempt from taxation. The IRS has clarified the student-employee exemptions, restricting its eligibility. There may be a few other rare exemptions, such as for the children of family-owned businesses. Some participants in state and local pension plans may also be exempt from Social Security tax. Some of these employees are not covered by Social Security, and therefore do not pay FICA taxes.

What Wages Are Subject To Medicare Tax?

Medicare tax applies to all taxable employment income. This includes a variety of income sources, including salary, overtime, paid time off, tips, and bonuses. There is no limit on the amount that is taxed; all taxable income is subject to Medicare tax. Medicare wages may exclude certain pretax deductions, while others are included. Pre-tax medical insurance premiums and contributions to a health savings account are not taxed. However, Medicare tax is assessed on retirement account contributions and life insurance premiums, despite the fact that these funds are exempt from federal income tax.

Medicare Premiums

If you never paid Medicare taxes it doesn’t mean you can’t sign up for Medicare when the time comes. It just means that you will have to pay a premium for Medicare Part A, which is normally free thanks to those Medicare taxes. As of 2023, if you don’t qualify for free Part A, the premiums can cost up to $506 a month. This also applies if you were unemployed for at least 10 years (40 quarters). Typically, you won’t be eligible for premium-free Part A insurance in this circumstance. However, if your spouse is eligible for free Part A and you meet citizenship and residency requirements you can also be eligible for free Part A.

FAQs

What is a Medicare deduction on my paycheck?

If Medicare is deducted from your paycheck, it indicates that your employer is fulfilling its payroll obligations. This Medicare Hospital Insurance tax is a mandatory payroll deduction that funds health care for seniors and individuals with disabilities.

What if my employer didn’t withhold FICA taxes?

Employers who violate tax laws by failing to withhold FICA taxes for Social Security and Medicare could face criminal and civil penalties. Check with your employer to ensure there was no error or that you did not claim exemption on your W-4 form if you discover that no taxes have been withheld. You may be required to pay a tax penalty at the end of the year if you underpaid.

What is a Medicare benefit tax statement?

This statement confirms that you are enrolled in Medicare Part A and have health insurance that meets the requirements of the Affordable Care Act. This form, also known as a 1095-B, can be used if the IRS requests verification of your health insurance coverage.

Working With EZ

Due to the Social Security and Medicare taxes, your net pay may not be as high as you would like. Nonetheless, these taxes provide you with retirement insurance. You can enroll in Medicare even if you have not paid enough Medicare taxes over your lifetime. Just be prepared to pay the Part A premiums that other seniors will receive for free. Medicare is beneficial, but it can be confusing. However, you will still need to make decisions regarding your healthcare after enrollment. Speak with an EZ representative who can explain everything and tell you how to sign up.

EZ can help you enroll in Medicare, purchase a Medicare Supplement Plan, or simply weigh your options. Our agents work with the nation’s top insurance providers. They can provide you with a complimentary comparison of all local plans. We will discuss your medical and financial needs and assist you in locating a plan that meets all of your specifications. Simply call one of our licensed agents at 877-670-3602 to get started.

Last year, there was new hope in the fight against Alzheimer’s disease when a new drug, Aduhelm, was approved for use to combat the disease. But now Medicare officials have announced their final decision to cover this drug only for people who receive it as participants in a clinical trial. This is good and bad news: while the drug won’t be as widely available, Medicare officials are considering cutting premiums for all beneficiaries, since the new drug was the reason for the $22 increase in Medicare’s Part B premiums this year.

The Price of Aduhelm

Aduhelm hit the market as the first new Alzheimer’s medication in nearly two decades, and many hoped it would be a breakthrough in fighting the disease. It was first priced at $56,000 a year, and was expected to generate billions for the company that developed it, Biogen. This astronomical price did eventually come down to $28,000 a year, but this price tag is still too high for Medicare.

Doctors have been hesitant to prescribe it, given the lack of coverage and weak evidence that the drug slows the progression of Alzheimer’s.

Insurance companies have blocked or restricted coverage.

Medicare Part B premiums have gone up $22 a month, the largest increase ever.

The Future Of Aduhelm

After all the concerns from insurers, doctors, and advocacy groups, Medicare decided to restrict the new drug, and only allow coverage for it for people involved in clinical trials. Dr. Lee Fleisher, the chief medical officer at the Medicare agency, explained this decision by saying that this way of dealing with the fast-developing field of Alzheimer’s therapies, a program called Coverage with Evidence Development, “is meant to be nimble and really respond to any new drugs in this class that are in the pipeline, and do demonstrate clinical benefit.”

But Medicare is also trying to make the trials accessible to more people: instead of requiring randomized controlled trials to be approved by C.M.S., Medicare will cover participants in any trial approved by the F.D.A. or the National Institutes of Health. This will allow the trials to be done in more locations, not just in hospital settings, and to include people with other neurological conditions like Down syndrome, many of whom develop Alzheimer’s but were not included in earlier trials.

Officials are hoping to lower Medicare Part B Premiums since the cost of Aduhelm has gone down.

In the trials, “the manufacturers will have to come to us with how are they going to include all patients that represent the Medicare population, and how are they going to ensure that all of these patients are getting appropriate medical treatment and monitoring of their treatment while they’re in each of these studies,” Tamara Syrek Jensen, the director of coverage and analysis for the Medicare agency’s Center for Clinical Standards and Quality, said in an interview.

Medicare Premiums

In the meantime, Medicare officials are in talks to hopefully lower Medicare Part B premiums now that they will not be covering Aduhelm for all Medicare beneficiaries, and now that the drug is coming down in price.

If you are one of the millions of Medicare beneficiaries who are living on a fixed income, saving as much money as possible is a top priority. The best way to save money on healthcare is to find an affordable Medicare Supplement Plan – and the best way to do that? Speak to an EZ agent! We work with the top-rated insurance companies in the nation and can help find a plan that will save you money this year – maybe even hundreds of dollars. Let our agents take the stress off you by comparing plans and finding ways to help you save money. And because we want to help you save as much money as possible, our services are completely free- no-obligation or hassle. To get free instant quotes for plans that cover your current doctors, simply enter your zip code in the bar on the side, or to speak to a licensed agent, call 888-753-7207.

The federal government has finally announced Medicare premiums for 2022, allowing beneficiaries a little over 3 weeks of budgeting time before the end of the Medicare Annual Enrollment Period (AEP). Medicare premiums are usually announced in late October or early November, but it has taken longer than normal to release the numbers this year, with officials blaming the pandemic and uncertainty over a new Alzheimer’s drug for the delay. So what kind of an increase can Medicare beneficiaries expect for the new year?

Medicare Part B Premiums

Unlike Medicare Part A (hospital insurance), Medicare Part B (medical insurance), which covers doctor visits, outpatient services, and medical equipment, has a monthly premium that increases each year. This year, there will be a 14.5% increase in Part B premiums, far outpacing an earlier estimate of 6.7%, which will take premiums for beneficiaries in the lowest income bracket from $148.50 a month to $170.10 a month. Officials at the Centers for Medicare and Medicaid Services (CMS) insist, though, that this increase will not be a burden on beneficiaries.

“Most people with Medicare will see a 5.9% cost-of-living adjustment (COLA) in their 2022 Social Security benefits—the largest COLA in 30 years. This significant COLA increase will more than cover the increase in the Medicare Part B monthly premium,” CMS said in a statement.

“Most people with Medicare will see a significant net increase in Social Security benefits. For example, a retired worker who currently receives $1,565 per month from Social Security can expect to receive a net increase of $70.40 more per month after the Medicare Part B premium is deducted.”

Medicare Deductibles

Medicare Part B Deductible

The Medicare Part B annual deductible will also see a big increase next year. It will increase by $30 from last year’s amount, making it $233 in 2022. That’s a 14.8% increase!

Medicare Part A Deductible

Medicare Part A does not have a monthly premium, but it does have an annual deductible; for 2022 it will be $1,556, up $72 from this year’s $1,484.

The cost of the new Alzheimer’s drug, Adulhem, is the cause for the increase in Medicare premiums.

Why the Delay and Why the Huge Increase?

CMS has said that part of the increase in premiums and deductibles is due to the uncertainty over how much the government will end up paying for the new Alzheimer’s drug, Adulhem. The drug, which was approved by the FDA in June, is the first Alzheimer’s medication in nearly 20 years and is estimated to cost about $56,000 a year per patient. That means if Medicare beneficiaries have to pay 20% of the cost of the drug, they would be facing $11,500 in out-of-pocket expenses just for this one medication. Medicare is still assessing whether they should cover the drug or not, and is hoping to have a decision by the spring. For now, Medicare is deciding on a case-by-case basis.

“The increase in the Part B premium for 2022 is continued evidence that rising drug costs threaten the affordability and sustainability of the Medicare program,” said Medicare chief Chiquita Brooks-LaSure in a statement.

These jumps in Medicare rates are the largest increases we have ever seen, so we understand that you’re worried about budgeting and being able to afford your medical expenses. The best way to better prepare for the 2022 rates is to find an affordable Medicare Supplement Plan – and the best way to do that? Speak to an EZ agent! We work with the top-rated insurance companies in the nation and can help find a plan that will save you money in the new year – maybe even hundreds of dollars. Let our agents take the stress off you and help you budget for the new year by comparing plans and finding ways to help you save money. And because we want to help you save more, our services are completely free- no obligation or hassle. To get free instant quotes for plans that cover your current doctors, simply enter your zip code in the bar on the side, or to speak to a licensed agent, call 888-753-7207.

Tax season is here! Are you still working on filing your taxes? And are you, like most people, looking for ways to get the biggest refund? If so, you should know that itemizing your deductions on your income taxes is the best way to get some money back; you should also know that medical expenses are one of the many things you can itemize. This is true for you even if you are enrolled in Medicare, as long as you know the restrictions and exactly what you can deduct.

Expenses You Can Deduct

There are multiple Medicare expenses that you can deduct from your income taxes.

If you didn’t know that you can deduct the cost of your Medicare premiums from your taxes, then you’ve been missing out on getting some of that money back. But that’s not the only Medicare expense you can deduct! If you want to deduct medical expenses, simply choose to itemize your deductions, and you can begin to claim:

Dental and vision expenses, including premiums, deductibles, and copayments

Lab tests

Hospital stays

Copayments

Any medication prescribed by your doctor

Medicare Part B premiums

Medicare Part A premiums only if you voluntarily enrolled in Medicare Part A and are not covered under Social Security.

Note that you can only deduct medical expenses that are more than 7.5% of your adjusted gross income, or AGI, for the year.

Medicare Supplement Plan

So, what about Medicare Supplement Plans? Can you claim the cost of these back? Having one of these plans can save you hundreds of dollars a year, but many taxpayers don’t realize that they can save even more money by deducting the cost of their Medicare Supplement Plan as a medical expense. The same note applies to these deductions: you can deduct any amount that exceeds a certain percentage of your adjusted gross income, usually 7.5%.

How To Deduct These Expenses

First, you will need to collect all of your receipts and add them up.

In order to deduct your Medicare expenses from your taxes, you will need to itemize deductions, not choose the standard deduction. To do this, gather all of your receipts for the year so you can determine how much you spent on medical expenses. Next, calculate 7.5% of your adjusted gross income, so you know how much you can deduct: remember, you can deduct any amount above that calculated amount. For example, if you have an adjusted gross income of $50,000, 7.5% of that amount is $3,750. That means, if you have a total of $7,000 in medical expenses, you can deduct $3,250 ($7,000 – $3,750 = $3,250).

Finally, once you have done all of these calculations, you will need to enter your qualified medical expenses on lines 1 through 4 on IRS Form 1040 or 1040 SR.

Medicare is great, but the truth is that it does not cover your medical expenses 100%. This is why the majority of seniors who enroll in Medicare also choose to purchase a supplemental insurance plan such as a Medicare Supplement Plan to cover what Medicare does not. These plans help older adults like you save hundreds of dollars each year, and you can deduct the premiums from your income taxes! If you are interested in finding out more about Medicare Supplement Plans, EZ can help. To compare plans for free, simply enter your zip code in the bar above, or to speak to one of our trained local agents, call 888-753-7207.

Big changes are coming for Medicare next year, affecting your coverage and wallet. Medicare Supplement plans C and F will disappear. Part B premiums and deductibles will rise. And for the first time since 2010, Medicare is changing the surcharges on high-income beneficiaries. Make sure you aware of all the changes ahead so you can make the necessary adjustments to fit both your needs and budget.

Part B

For 2019, the standard Medicare Part B premiums are $135.50 a month. Next year’s increase is projected to be about $144.30 a month.

Many seniors depend on Social Security to help pay for their premiums. For 2020, Social Security’s COLA, or cost of living adjustment, is expected to be about 1.6%. This would increase the benefit to $23 a month, which will in turn cover the increase in Part B premiums.

The Part B deductible was $185 in 2019, and is now projected to increase to $197. In order to help pay for the deductible, Medicare beneficiaries will be forced to sign up for a Medicare Supplement plan.

Medicare Supplement Plans C and F

As mentioned, Medicare Supplement plans help beneficiaries pay for their Part B deductible. Plans C and F will no longer be available for purchase by newly-eligible Medicare beneficiaries.

As long as the beneficiary is enrolled in Medicare before 2020, they can keep their plan C or F, or can apply for them at a later date. These two plans are popular plans because they are the only ones that cover the Part B deductible in full.

Medicare Surcharges

With these monthly payments, Medicare covers 80% of charges, and the other 20% is up to the beneficiary. Some seniors have a higher income than others, and as a result, they also pay a higher price.

This higher price is referred to as a “surcharge”. The surcharges are imposed because these higher-income beneficiaries can afford to pay more for healthcare. The surcharge is called IRMAA, which stands for Income-Related Monthly Adjustment Amount.

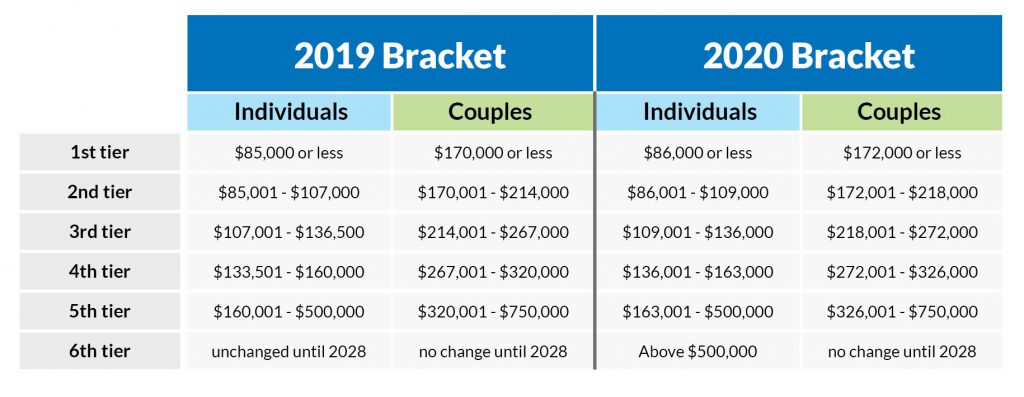

For the past couple of years, high-income beneficiaries were in the set income bracket of $85,000 for an individual, and $170,000 for a married couple. Starting in 2020, the income brackets will be adjusted for inflation.

2020 Medicare Surcharges

The surcharge will now apply for those making an income of $87,000 as an individual, and $174,000 for a married couple. Premiums in 2019 range from $189.60 a month to $460.50 a month, depending on income. For 2020, these amounts are projected to range from $202 a month to $490.50 a month, depending on income.

The Centers for Medicare and Medicaid Services have not announced the actual increase in Part B premiums and deductibles yet. However, the projections are enough to make a Medicare beneficiary prepare for the upcoming changes. Seek out any Medicare Supplement plans you might want to get, especially if it is plan C or F.

Do not be in disarray or panic about the changes ahead. If you are enrolled in Medicare, signing up for a Medicare Supplement plan does not have to be a hassle. EZ.Insure can take care of the research of all the plans within your region, provide you with the best options that meet your coverage and price, and sign you up. You will be given your own personal agent who is highly trained within your region. We offer you all of these services for free! To get started, simply enter your zip code in the bar above, or to speak with an agent, email [email protected], or call 888-753-7207.

This past October, the CMS released the new rates for Medicare deductibles and copays for 2019. It is important to review the new rates to determine if it is affordable for you and your situation. If you can not afford the raised rates, then now would be the time to make some budget changes, or consider a Medicare Supplement plan. Most, if not all, Medicare Supplement plans will cover the deductibles and copays.

The New Rates

Medicare Part A Hospital Deductibles have gone up $24 from 2018. It is now $1,364.

Medicare Part A Deductible for a Skilled Nursing Facility for days 20-100 have gone up $3 per day since last year. The cost is now $170.50 per day.

Medicare Part B Deductible has gone up $2 from 2018. It now costs $185.

Medicare Part B Premiums have gone up $1.50 from 2018. Premiums will be $135.50 a month.

Annual income rates have increased; if your income was greater than $85,000 single or $170,000 couple, then you will face additional costs for Medicare Part B premiums. About $2.10 more a month.

2019 Medicare premiums are going up based on income.

The day before the Medicare rates were announced, the Social Security Administration had its own announcement. The Administration set a 2.8% cost-of-living adjustment, COLA, to 2019 social security benefits. Thanks to the “hold harmless” provision, almost 2 million Medicare beneficiaries will not have to pay the full Part B monthly premium payments of $135.50. Hold harmless is the guarantee that a Medicare beneficiary receives limiting how much their Part B premiums can go up. The premiums can not be greater than the increase in their Social Security benefits. However, this only applies to 3.5% of Medicare beneficiaries. So what are the rest to do?

Plan Ahead

If you can not budget the new Medicare premiums for 2019, then a Medicare Supplement can help.

Even though the costs have increased only by a couple of dollars a month, the $2 can add up throughout the year. It can change the budget for a lot of people, and some will be struggling to fit it into their budget. If you are one of these people who worry how you are going to pay these extra costs, then looking into a Medicare Supplement plan would be beneficial. There are 10 different kinds of Medicare Supplement plans that you can look into. Most of these plans will pay the deductibles and copays, and offer extra benefits that Original Medicare does not offer.

Researching and comparing the different kinds of Medicare Supplement plans can be frustrating. EZ.Insure offers highly trained agents in your region that specialize with Medicare Supplement plans. They can go over your needs with you, compare plans, and provide you with quotes instantly. To get a quote enter your zip code in the bar above, or contact an agent by calling 888-753-7207, or emailing[email protected]. We make the process easier for you, so you do not have to stress or miss an important detail.

When the Medicare tax was first introduced in 1966, the tax rate was 0.7% of an employee’s wages, with the employer and employee each paying 0.35%. The rate has since gone up considerably. In 2023, the Medicare tax rate is 2.9% which is still shared equally between the employer and employee. W-2 employees pay 1.45% towards the Medicare tax and their employer covers the remaining 1.45%. Self-employed individuals must pay the full 2.9% in full because they are both the employee and the employer.

When the Medicare tax was first introduced in 1966, the tax rate was 0.7% of an employee’s wages, with the employer and employee each paying 0.35%. The rate has since gone up considerably. In 2023, the Medicare tax rate is 2.9% which is still shared equally between the employer and employee. W-2 employees pay 1.45% towards the Medicare tax and their employer covers the remaining 1.45%. Self-employed individuals must pay the full 2.9% in full because they are both the employee and the employer.