Health Reimbursement Arrangements (HRAs) and Health Savings Accounts (HSAs) are both great options for employees and employers who want to save money on group health insurance costs. Many employers and employees wonder if they can have both at the same time, and the answer is: yes! If you are willing to offer your employees both, a HRA and HSA, you need to have an understanding of how the two benefits interact with each other in order to get the most out of each.

The Difference Between HSAs & HRAs

HSAs are savings accounts that work alongside your employees’ health insurance plan. Employees are only eligible for a HSA if they are enrolled in a qualified high-deductible health plan. Your employees can contribute money to the account, which then acts like a bank account for medical expenses; you can also contribute to their HSAs, and receive some of the tax benefits. The money that you both contribute is pre-tax, earns tax-free interest, and will not be taxed when employees withdraw it to use for qualified medical expenses.

HRAs are not savings accounts like HSAs, they are arrangements that allow employers to reimburse employees for medical expenses. They are intended to help employees pay for out-of-pocket health-related expenses, and are often used in place of a traditional group health insurance plan. Depending on the type of HRA you offer, there may or may not be a limit on the amount that you can reimburse your employees in a given year.

The Different Types of HRAs

First, let’s take a look at the different types of HRAs you can offer your employees. There are integrated HRAs, which are offered alongside traditional group health insurance, including:

There are 5 different HRA types to choose from to offer your employees.

ICHRAs (Individual Coverage Health Reimbursement Arrangements), whichallow tax-free reimbursement of benefits for any size business, and for any amount.

EBHRAs(Excepted Benefit HRAs), whichare limited to paying for excepted benefits, such as premiums for vision and/or dental coverage and premiums for plans that are exempt from ACA rules (short-term plans).

Standalone HRAs do not have to be tied to a group plan. These include:

QSEHRAs (Qualified Small Employer HRAs) – These are meant for businesses with less than 50 employees that do not offer a group insurance plan. Business owners can set up a QSEHRA for their employees to help pay for benefits tax-free.

Spousal HRAs– These are for employees who are covered by a spouse’s group plan. They cannot be used to reimburse employees for their premium payments.

Retiree HRA– These are for former employees. They allow you, the employer, to help pay for any retired members’ insurance premiums and medical expenses.

When Offering Both HSAs & HRAs

In order for your employees to be eligible for a HSA, they must have a high-deductible health insurance plan (HDHP) that is HSA-qualified. If you choose to offer a HRA and a HSA, then the HRA has to follow the same rules as a HDHP, and cannot begin paying out until your employee’s minimum “deductible” amount is met.

Limited-purpose HRAs will reimburse employees for expenses exempt from HSA deductible, such as dental work.

Another way to offer a HRA that is HSA-qualified is by offering a limited-purpose HRA that only reimburses employees for expenses that are exempt from the HSA deductible requirement. Expenses exempt from the HSA deductible are:

Health insurance premiums

Dental

Vision

Long-term care premiums

Wellness and preventive care such as check-ups and quitting smoking or weight loss programs

You want to help your employees with their healthcare costs, but there is nothing wrong with also wanting to offset the costs of group health insurance. One way to do this is by offering both a HRA and a HSA. It can be done! As long as you follow the guidelines, then everyone can benefit from these arrangements. If you are unsure or need some help, then we can assist you. To compare plans, and to find a plan with the most coverage and savings, enter your zip code in the bar above. Or to speak directly to one of our licensed agents, call 888-998-2027.

Employers who have trouble providing their employees with a traditional group health insurance plan sometimes turn to health reimbursement arrangements (HRAs) to help. HRAs are not health insurance, they are employer-funded accounts approved by the IRS that help employees pay for qualified out-of-pocket medical expenses. They can also help pay for their individual health insurance plan’s premiums. HRAs work through a reimbursement system. Employers offer employees a monthly allowance of tax-free money that they can use to pay for healthcare services, including health insurance, and then the employer reimburses them up to their allowance amount. But what if you’re a sole proprietor? You can offer this arrangement to any employees you have, but can you participate in the savings from an HRA yourself? In short, generally no, but there is a way you might be able to!

Offering an HRA is a great way to help pay for your employees’ healthcare costs; these arrangements give you more control over how much you’re spending, and can help to lower your healthcare costs. HRAs only need to be funded when employees who participate in them incur expenses, and not all employees who participate will incur expenses up to the limit established by the employer. Any unused funds in the HRA stay with you, the employer.

There are also tax advantages to HRAs: any reimbursements made to your employees are tax deductible for you and tax-free for your employees. HRAs are only available to:

Current and former employees, and their spouses.

Covered tax dependents.

Children who will not be 27 years old by the end of the tax year.

Unfortunately the IRS does not separate you and your business, which makes you ineligible to participate in an HRA.

Sole Proprietorship

As a sole proprietor, according to the IRS, there is no separation between you and your business. The Internal Revenue Code Section (IRC) 401(c) determines that owners who are self-employed individuals are not considered employees. This makes them ineligible to participate in a HRA. Ineligible owners include partners, sole proprietors, and more-than-2% shareholders in a Subchapter S corporation.

However…

If you are married and your spouse is listed as a W-2 employee at your business, then there is a way for you to get a HRA, and enjoy all of its tax benefits. To work around the rule set by the IRS, you can set up a HRA in your spouse’s name and list yourself as a dependent of your spouse. However, this will only work if you don’t hire any other W-2 employees who would be eligible for either an ICHRA, QSEHRA or a One-Person 105 HRA. What you can do is:

Hire your spouse as a W-2 employee, and make their salary the amount you want to reimburse through the HRA.

Make your spouse the primary policy holder on your family health insurance plan.

Become a dependent on your spouse’s health insurance plan.

Set up a One-Person 105 HRA, ICHRA, or QSEHRA for your spouse. Consider:

The One-Person 105 option if you have medical expenses or other employees that are excludable under the rules.

A QSEHRA if your health expenses are less than the reimbursement limit under the QSEHRA rules.

An ICHRA if the reimbursement limit of a QSEHRA is too restrictive, since there are no limits on ICHRA contributions.

Save all of your medical bills so your company can reimburse them each month from a separate account.

Get Help

To make sure that you are following the rules laid out by the IRS properly, it would be wise to speak with an insurance agent. EZ’s agents are highly trained and knowledgeable in the group health insurance industry, and can help you determine if participating in an HRA is possible for you. To find out if you are eligible, and to compare plans in your area for free, enter your ZIP code in the bar above, or to speak directly to an agent, call 888-998-2027.

Being a small business owner means being on a tight budget, so fitting in a group health insurance plan for your employees can seem a bit overwhelming. Offering group health insurance, though, is not something that you should overlook. If you do not offer a healthcare plan, you might find that it is more difficult to recruit and retain good employees. In fact, surveys show, most employees say that they would prefer to be offered health insurance over a pay raise. While group health insurance can seem unaffordable or unattainable, providing healthcare has many advantages that can balance out the costs – and there are ways to get great plans at an affordable price.

Tax Credits & Deductions

Contributing to your employees’ premiums can be expensive, but you can get some of that money back through tax credits and deductions. If you run a small business, you might qualify for the small business health care tax credit if you offer your employees a plan through the Small Business Health Options Program, or SHOP. To qualify for the minimum credit, you must have fewer than 25 full-time or full-time equivalent employees earning an average of $50,000 or less per year; to qualify for the maximum credit, you must have fewer than 10 employees earning an average of $25,000 or less per year.

If you decide to offer a HRA or HSA, your employees will get tax advantages (all of their contributions and reimbursements are pre-tax), and so will you. Contributions to your employees’ HSAs and HRA reimbursements are tax-deductible.

Lower Payroll Taxes

Another tax benefit of offering group insurance is the ability to lower your payroll tax. When employees pay for health insurance, the cost of their premiums is typically excluded from their taxable income. This lowers most workers’ tax bills, and in turn reduces their after-tax cost of coverage. Lower taxable income for your employees means lower business payroll taxes for you. In addition, if you contribute to your employees’ HSAs, you can also save on payroll taxes because HSA contributions are deducted from your payroll on a pre-tax basis.

You and your family can participate in your group insurance plan.

You Can Participate In The Plan

Offering health insurance to your employees means that you and your family can also participate in the plan. Compared to individual plans, group policies offer more pre-deductible benefits such as preventative care and primary doctor visit coverage. They also offer lower copays for prescription drugs and routine care.

Lower Costs Due To Larger Risk Pool

The higher the number of employees that participate in your group plan, the lower the cost of health insurance. When more people are included in your plan, you have a larger risk pool, and everyone will have more options at a lower price.

Do you want healthy, productive employees who show up to work and boost your bottom line? Then provide them with group health insurance! If you want employees who come to work and work hard for you, there’s no better way to ensure you’ll get that than by offering health insurance. They’ll be able to receive care when they need it, and they will feel like you have invested in them, so they will invest in you. This will lower your hiring costs, improve morale, and reduce absenteeism and risks associated with poor health.

Health insurance can help you keep your current employees happy and healthy, and it can also help you to attract the best employees when it comes time to hire. Job seekers expect employers to offer health insurance and partially pay for their premiums, so you risk missing out on great candidates and potential employees if you’re not offering some sort of plan. You don’t want to be disappointed if a candidate rocks the interview, you offer them the job, and they turn it down because you’re not offering the benefits they’re looking for!

When searching for a group health insurance plan, you have to look beyond the premium. The costs associated with group health insurance plans include premiums, which you contribute to, but also co-payments, deductibles, and coinsurance, which your employees are responsible for. If you are looking for a way to lower your premium costs, consider offering a high deductible health plan. The higher the deductible a plan has, the lower the premium costs will be, so you can save on contributions. You can also offer a HSA with qualified high deductible health plans, so your employees will be able to put money aside to help with the cost of the higher deductible.

Affordable group health insurance plans are out there, and you can find the right one for your business as long as you use a licensed, trained agent to help you. There are ways to offer everyone the most coverage while saving the most money. The best way? Start by talking to an EZ agent! All of our services are completely free, and there’s never any hassle or obligation. To instantly compare plans in minutes from top rated carriers around the country, enter your zip code in the bar above, or to speak directly to one of our agents, call 888-998-2027.

If you own a business that employs fewer than 50 people, then you are not required to offer your workforce group health insurance – but that doesn’t mean that you can’t, or that you shouldn’t. Many small business owners find that having healthier and happier employees is worth the cost and the administrative headaches of providing a healthcare plan, some go even further: they offer multiple plan options for their workers to choose from. Going this route may not be right for every small business, but if you’re looking to keep a diverse workforce satisfied, then it might be right for you.

Employees prefer health insurance over a raise in pay, and it is a huge deciding factor for job seekers.

Offering Health Insurance: The Stats

If you’re not currently offering a healthcare plan to your employees, you may want to take a look at a few stats:

40%: The percentage of workers that say that healthcare is their number one priority when it comes to benefits.

88%:The percentage of job seekers who say that they would give health benefits “some consideration” or “heavy consideration” when choosing a job. 46% said it was a deciding factor.

56%: The percentage of people with employer-sponsored health benefits who say that whether or not they like their health coverage is a key factor in deciding to stay at their current job.

50-60%of a worker’s annual salary: The amount it can cost to find a direct replacement for them if they leave their position.

$4,000: The average amount it takes to hire an employee.

The numbers above should give you an idea of how important offering group insurance to your employees can be to recruiting, retention, and to your bottom line. Adding flexibility to your plan options can only increase those benefits.

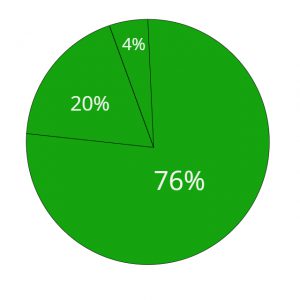

Percentage of employees who offer one or more plans to their employees. 76% offer 1 plan type.

If you are currently offering one type of insurance plan to your employees, then you’re not alone. According to the Kaiser Family Foundation 2019 Health Benefits Survey:

76% of small businesses offer one plan type

20% offer two plan types

4% offer three or more plan types

If you’re choosing between plan types, you might want to take a look at a breakdown of what other small employers are choosing:

Point of Service (POS) plans: almost half of small employers – 47% – chose this option, according to a recent survey. POS plans are a hybrid of PPOs and HMOs: they have the lower premiums and primary care physician requirement of HMOs, but are slightly more flexible.

HMOs:This type of plan, which requires that employees choose a primary care physician, get referrals to see specialists, and stay within a narrow network, accounted for 26% of small business plans

PPOs: 15% of plans were this more flexible type, which have larger networks and fewer requirements than an HMO, but also have higher premiums.

Offering Plan Options: The Factors

Now that you know all the relevant facts and figures, and we’ve established that offering at least one plan is a good idea, let’s take a look at the factors that should go into determining whether you decide to offer more than one plan type.

The ages and health needs of your employees: If you’ve got a workforce completely populated by Millennials or X-ennials who are single, childless, and healthy, then offering a one-size-fits-all high deductible health plan might be a great choice for you. You and your young, healthy employees could both save money on premiums, and they could contribute money tax-free to an HSA. But if you have some older employees, or employees who need to visit their doctor often, then they would probably prefer a plan with a higher premium and lower deductible. Adding a PPO into the mix would probably work for them, especially because they might not want to have to see their primary care physician every time they need to visit a specialist.

Location: If your employees all live and work in one small area, then they might not need to pay extra for a PPO with a wide network. However, if you have a lot of commuters who are spread out over a large area, they may prefer the flexibility of a plan with a larger network.

Budget:You need to think about what both you and your employees can afford when it comes to choosing a plan. If you really can’t find it in your budget to contribute to higher premiums plans, then stick with offering a cheaper option – it’s better to offer one plan than no plan! On the other hand, if most of your employees are older and/or have families and are willing to pay for a more full-coverage plan, but you have a few younger, more budget-conscious employees, consider offering them a second, cheaper option.

There’s always a lot to consider when choosing whether – and how – to offer health insurance to your small business’s employees. If you need more input, turn to your employees themselves – you can always offer an anonymous employee healthcare survey so that they can tell you exactly what they want. And if you need still more help, turn to EZ! We can answer all of your questions about offering multiple plans (or anything else!), find you the best plan options, and get you super fast, accurate quotes, and we’ll do it all for free. To get started with us today, simply enter your zip code in the bar above, or to speak with an agent directly, call 888-350-1890.

Starting a small business is a great accomplishment! It takes a lot of hard work, and you probably have a to-do list a mile long. One very important thing on your list should be finding a great group health insurance plan. Offering health insurance to your employees leads to so many advantages for your business, like healthier, happier employees who are more likely to stay in their jobs, and tax breaks for you. There are many high-quality affordable plans to choose from, but you might be wondering where to begin, and you’ll probably have a lot of questions as you search for the right one for your business and your employees. That’s where EZ comes in: we’ve also got the answers to your most frequently asked questions and can give you a free quote to help you compare local group health insurance plans from all of the top carriers.

An agent will be able to offer you exclusive deals and promotions from insurance companies.

Both insurance brokers and insurance agents act as the middlemen between insurance buyers like you, and insurance companies. Using an insurance agent, like one of EZ’s, is the best option for small business owners looking to purchase a healthcare plan. Agents can expedite the buying process, they have specialized knowledge about the policies they sell, and they can keep you up-to-date on any changes to your plan. Our agents also have access to exclusive products from the top-rated insurance companies, which can save you more money than if you go it alone.

What is the minimum number of employees to get a group plan?

If you have 50 or more full-time employees, you are required to provide health insurance or you will be penalized under the employer mandate of the Affordable Care Act. You are eligible for a group plan as long as you have 2 full-time (or full-time equivalent) employees, including yourself. Full-time employees are considered those who work 30 hours or more a week.

The 2-employee rule is always true for tax-advantaged small business health insurance options program (SHOP) plans (although you will need 70% participation in your plan). If you’re looking into other group plans, some insurance companies may have different requirements. Ask one of EZ’s agents to check for you.

What is the average cost for a group health insurance plan?

Small business health insurance costs are determined by your location, number of employees, and how much you would like to contribute to your employees’ coverage. The average cost of annual premiums for employer-sponsored health insurance was $7,188 for individual coverage and $20,576 for family coverage in 2019. The average annual deductible amount for individual coverage was $1,655 for covered workers.

SHOP plans, as mentioned above, can offer some savings through the small business health insurance tax credit, if you have fewer than 25 full-time employees and meet certain requirements. Speak with an EZ agent about this possibility, or use our online tool to check fast, no-cost quotes for all available plans. We can help cut costs – but not benefits – by comparing multiple plan options.

How do I communicate the new benefits to my employees?

Simple, just ask your EZ agent! EZ’s agents are experienced in helping you communicate new benefits to your employees. Our agents will provide a Summary of Benefits Coverage (SBC) to participants and their beneficiaries before enrollment in the plan, at renewal of the plan, within 90 days of a Special Enrollment, and within 7 business days of a written request. They will also help you provide each employee covered under the plan a Summary of Material Modification (SMM) when there are changes made to their health benefits.

How much do I charge employees to be on the plan?

Employers are required to contribute at least 50% of their employee’s health insurance premiums, but you can contribute more.

Employers are required to contribute at least 50% of each employee’s health insurance premiums. On average, employers contribute approximately 82% of individual insurance premiums, and around 71% of family plan premiums. The more that you contribute to your employees’ premiums, the more likely employees are to enroll, and the more you will save – and don’t forget all of these contributions are tax-deductible!

You have options when it comes to plans and premium prices, so talk to an EZ agent about what’s best for you and your employees. For example, if you choose a plan with a low deductible, but higher premium, you may not be able to contribute more than 50%, and your employees might find it too expensive to enroll in your plan. In this case, you might want to look into a high deductible health plan, which would allow your employees to contribute to a health savings account (HSA). An EZ agent can help you determine how much you can afford to contribute, and other ways you can save!

Will offering health insurance help me attract better employees?

Businesses that offer health insurance tend to attract and recruit the best candidates. Most job seekers won’t even look twice at a posting if an employer does not offer health insurance – job seekers want to know that a prospective employer is willing to invest in them. Surveys show that 46% of job seekers said that healthcare was a deciding factor in taking a job, and that 60% of employees would take a job with lower pay but better benefits.

Will my employees be happier if they have health insurance?

Offering health insurance can mean having more loyal employees and a lower turnover rate. 83% of employees say health insurance is extremely important when deciding whether or not they should change jobs. Employees with health insurance are happier, less likely to leave their jobs, and healthier.

One survey found that 72% of employees said having more work benefits would increase job satisfaction. Knowing that they will be protected in case of an emergency, that their chronic conditions will be covered, and that they will not have to worry about large medical bills, means less stress for them and more productivity for you.

Will productivity go up if we offer health insurance?

Absolutely! In one recent study, 60% of employers said that offering health insurance led to higher productivity levels at their businesses. Not only will offering health insurance to employees lower their stress levels, but it will also keep them healthy – and healthier employees are less likely to take time off for being sick. When you invest in your employees, you’re boosting your bottom line.

What other benefits should I consider offering?

Offering telemedicine to your employees is a great benefit that can help you save money.

When choosing a plan, look at what “extra” benefits it offers – for example, telemedicine. This convenient option can actually save you thousands due to the reduced cost of healthcare claims from unnecessary visits to the doctor and reduced visits to the emergency room. It is more convenient (and less expensive) for employees to call and speak with a doctor to receive care.

You can also consider offering a workplace wellness program. These programs help keep healthcare costs down by giving incentives to employees to live healthier lives. These programs can include things like health screenings, programs to quit smoking, gym membership stipends, diet and weight loss programs, or diabetes management programs. To find out what extra benefits you can offer, talk to an EZ agent.

How will I know if my doctor and my employees’ doctors are in-network?

If you are looking for a plan that includes specific doctors, speak to an EZ agent to find a plan that includes the best network for you and your employees. Our agents can easily access any insurance company’s networks and included providers in minutes.

If you already have a plan, check your plan info to see if there’s a list of covered doctors. You can also call your doctor’s office, ask for their tax ID number, and then call your insurance carrier to find out if they are covered. Or you can avoid this long and annoying process by simply asking one of EZ’s agents to check for you!

EZ.Insure understands how time consuming and overwhelming finding a group health insurance plan for your small business can be. To make the process easier, we provide you with a personal agent who will answer all of your questions, compare plans, and provide you with free, instant, and accurate quotes. We do all the heavy lifting for you so that you can provide the best insurance for your employees, without breaking the bank. Let us help you save time and money. To get started, enter your zip code in the bar above, or to speak to a specialized agent within your area, call 888-998-2027.

Health insurance is expensive. And frustrating. Especially if you’re someone who is self-employed and does not have any employees. Until recently, if you were in this boat, then you were stuck getting insurance on the individual ACA marketplace, which could be very expensive if you didn’t qualify for any subsidies. But now, thanks to a relatively new rule surrounding Association Health Plans, you have a way to get more affordable group health insurance even if you don’t employ anyone else, or are as casual and unincorporated as a handyman or tutor.

What are Association Health Plans?

Association Health Plans (AHPs) have existed for decades, and are basically a way for small businesses to get affordable healthcare. Even though they have the word “plan” in them, they are not healthcare plans. Instead, an AHP refers to a large group of small businesses and sole proprietors banding together to increase their insurance purchasing power.

The small businesses in an AHP may all be in the same industry or the same geographical location, but either way, they can use their combined size to get healthcare coverage as if they were one large employer. For an insurance company, the larger the pool of people they are insuring, the less of a risk it is – so they can charge less per person.

Once you join, AHPs function much like traditional insurance. You will get the familiar insurance card and will have access to the insurance company’s set network of healthcare providers. Premiums will be set the same way they are with all insurance plans – AHPs could, at one time, use a small group’s health status to decide how much to charge, but they are no longer allowed to do so. However, unlike ACA marketplace plans, with AHPs there are no metal tiers to choose from, and AHPs can also choose to be more flexible with their enrollment periods than ACA plans.

Working Owners

You don’t need to have a formal, incorporated business to be a “working owner”: you can do handyman work.

Up until 2018, only small businesses that had employees were able to join AHPs. But, following an executive order signed by President Trump in 2017 (and some legal battles over new AHP rules), people now defined as “working owners” can also join AHPs. These “working owners” can also get coverage for their spouses and dependents through AHPs.

When it comes to AHPs, a “working owner” is seen as someone who is both an employer (since employers are the ones who can become members of AHPs) and an employee who can use the AHPs insurance plan. And you don’t need to have a formal, incorporated business to be a “working owner”: you can do handyman work, teach piano, drive for a ridesharing company, or tutor students in your spare time. Even if you have a regular full-time job, but don’t have health insurance, you can join an AHP based on your “side hustle.” To become a member of an AHP, you simply have to be earning money from the work you are doing and meet oneof the following criteria:

Work for an average of 20 hours per week or 80 hours per month as a sole proprietor or self-employed person. You can spread these hours over multiple paid, self-employed activities

Earn as much as the cost of the plan coverage for the working owner and any other dependents added to the plan

The Disadvantage of AHPs

If you are a sole proprietor, or someone working at multiple unincorporated side jobs, and have been struggling to find affordable insurance, the possibility of being able to access group health rates can seem pretty exciting. But there are definitely critics of AHPs. Some claim that they weaken the entire ACA by drawing young, healthy people away from the marketplace, leaving older, sicker people to drive up prices.

AHP plans can base their premium rates on gender and other factors.

But even if the stability of the ACA marketplace doesn’t worry you, you might be concerned about the main disadvantage for those getting an AHP policy: AHPs don’t always provide full coverage. Under the new rules surrounding them, AHPs are now treated like large employer policies and, as such, they do not need to follow a lot of the rules of ACA plans. The premiums may be cheaper, but the savings sometimes come at a price: large employer policies (and AHP policies) do not need to cover the ten essential benefits that ACA plans need to cover.

AHP plans can also base their premium rates on age, gender, and industry. So, in addition to worrying about whether you’re getting the coverage you need, you also need to check into how each plan is priced and make sure you’re getting the best deal.

Health insurance can seem like a wild, wild world sometimes. So much to know, so many possibilities, and so many pros and cons. While you may be going it alone in your job, you don’t need to go it alone when searching for the right plan for you. EZ.Insure is here to help and will offer you your own knowledgeable agent who can help you sort through all of the noise. We’ll get you instant quotes for free, so get started with us today. Simply enter your zip code in the bar above, or to speak with an agent directly, call 888-350-1890.

HRAs work through a reimbursement system. Employers offer employees a monthly allowance of tax-free money that they can use to pay for healthcare services, including health insurance, and then the employer reimburses them up to their allowance amount. But what if you’re a sole proprietor? You can offer this arrangement to any employees you have, but can you participate in the savings from an HRA yourself? In short, generally no, but there is a way you might be able to!

HRAs work through a reimbursement system. Employers offer employees a monthly allowance of tax-free money that they can use to pay for healthcare services, including health insurance, and then the employer reimburses them up to their allowance amount. But what if you’re a sole proprietor? You can offer this arrangement to any employees you have, but can you participate in the savings from an HRA yourself? In short, generally no, but there is a way you might be able to!